The IRS has FAQ sections on its Foreign Account Tax Compliance Act (FATCA) website that respond to issues a taxpayer might have in attempting to comply with the various requirements. This includes a section that covers general issues as well as a section that covers issues faced by a Qualified Intermediary (QI), Withholding Foreign Partnership (WP) and Withholding Foreign Trusts (WT). Some of these have been revised or updated recently and may have an impact on foreign taxpayers who deal with financial and non-financial transactions with US source payor. The following are some of the pertinent changes:

FATCA-FAQs General:

FATCA Certifications

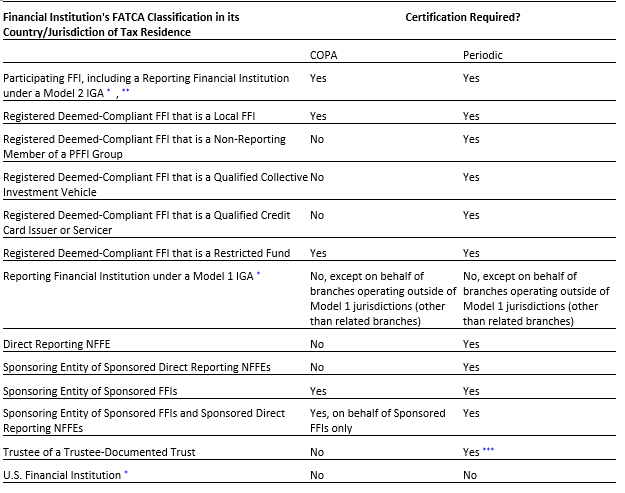

Q2. I am an entity that is registered on the FATCA registration system and that has been issued a GIIN. Do I need to submit a FATCA certification?

The answer generally depends on your FATCA classification. Not all entities are required to submit either or both types of certifications. The table below provides a general overview of the types of entities that are required to certify and which certification(s) they must submit. For more specific guidance, see Section 8 of Revenue Procedure 2017-16, the Treasury regulations, or an applicable intergovernmental agreement (IGA).

|

Compliance FIs may make the COPA and periodic certifications on behalf of electing FFIs that are part of the compliance FI's consolidated compliance program. A compliance FI may have one of the following three FATCA classifications: (1) Participating FFI, including a Reporting Financial Institution under a Model 2 IGA; (2) Reporting Financial Institution under a Model 1 IGA; or (3) U.S. Financial Institution. |

|

|

A participating FFI that is an electing FFI of a consolidated compliance group will be included in the certification of the compliance FI. |

|

|

A periodic certification of compliance is required only for a Trustee-Documented Trust that is subject to a Model 2 IGA. |

Q13. When are the FATCA certifications due?

For the certification period ending December 31, 2017, FATCA certifications are generally due no later than December 15, 2018; however, for sponsoring entities and trustees of a trustee-documented trusts, they are due no later than March 31, 2019.

Qualified Intermediary (QI), Withholding Foreign Partnership (WP) and Withholding Foreign Trust (WT)

Certification and Periodic Reviews

FAQ 2: How should the independence standard for an external reviewer of a QI, WP or WT be applied for periodic review years before 2019?

The IRS says that, for review years before 2019, the agency will permit an external reviewer of a QI, WP or WT to apply the standards of independence that would otherwise apply to its engagement to conduct the periodic review (such as the standards for an agreed-upon procedures engagement by a CPA). The IRS intends to update this FAQ to provide further guidance on the independence standard for reviews of calendar years 2019 and later.

FAQ 5: How should a group of QIs or WPs apply to form a consolidated compliance group (CCG)?

The IRS says that, for certifications due in calendar year 2019, an application to form a CCG should have been submitted by the responsible officer (RO), or other authorized user of the proposed Compliance Entity, no later than April 1, 2019. Such a submission must be made using the QI/WP/WT Application and Account Management system.

If you missed the deadline, FAQ 5 still contains useful information for future applications. That is, upon submission of an application to form a CCG, the IRS will contact the applying Compliance Entity to request any further information necessary to determine whether the CCG is acceptable to the agency. This ongoing discussion will also address issues such as the final composition of the group members and sample design for any statistical sampling to be used for the periodic review.

FAQ 18: What’s the deadline for QI/WP/WT entities, with a certification date of July 1, 2019, to select the periodic review year of their certification?

The IRS says all QI/WP/WT entities with a certification due date of July 1, 2019, must have selected the periodic review year of their certification period by July 1, 2019. This includes entities with an effective date later than January 1, 2015, and earlier than January 2, 2016. It also includes those entities selecting 2018 as their periodic review year. This FAQ doesn’t apply to termination certifications.

If you have questions concerning the above or have missed any of the deadlines, we would be pleased to discuss your options and possible actions you should consider at this time.

Thank you.