On March 5th, 2019 the IRS released the latest installment of proposed regulations (the “Proposed Regulations”) to address the Section 250 deduction. One part of the Section 250 deduction allows a taxpayer a deduction for Global Intangible Low-Taxed Income (“GILTI”) in the amount of 50 percent. This potential reduces the negative impact of the GILTI provisions by half.

The Proposed Regulations offer some very welcome guidance for individuals who are US Shareholders in Controlled Foreign Corporations (“CFCs”). Prior to the guidance, there was uncertainty about whether an individual electing Section 962 treatment would receive this deduction similar to corporations that owned foreign corporations. This allows individuals to have Subpart F income (including GILTI) to be taxed at the US corporate rate and to avail themselves of the Section 250 deduction. The Proposed Regulations confirm that the Section 250 deduction will, in fact, be available for individuals.

The Section 962 election allows for the Subpart F income (including GILTI) of an individual to be taxed as if the income was received by a corporation at the corporate tax rate (currently 21 percent). Since the income is taxed “as if” it was received by a US corporation, a Section 960 Foreign Tax Credit (“FTC”) is available to offset the tax imposed on Section 962 income. Subsequent distributions of the non-excludable Section 962 earnings and profits (“Section 962 E&P”) are not tax-free like normal Subpart F income but are included in the gross income of the recipient. This election may eliminate current tax due to the ability to claim a FTC on Section 962 income resulting in deferral of US tax until an actual distribution of the income to the USSH.

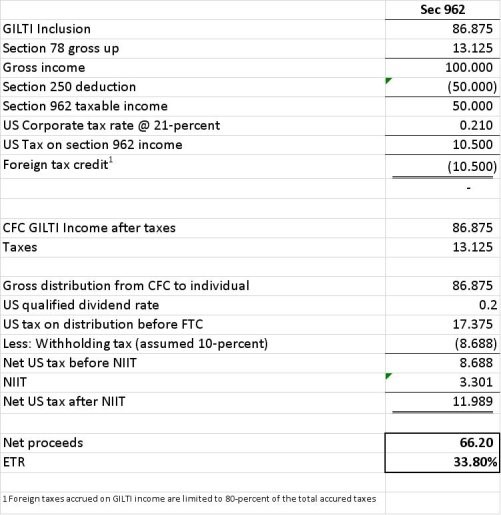

Where the tax rate in the jurisdiction of the CFC exceeds 13.125 percent, the net result of such an election will not only defer the taxation of the income but may also result in converting ordinary income taxed at a rate of 37 percent into qualified dividend income at a rate of 23.8 percent as shown in the example below:

Facts

Individual 1 owns a 100 percent interest in CFC 1, a qualified foreign corporation. CFC1 has gross income of $100 and pays tax of $13.125, resulting in GILTI income of $86.875[1]. During the same year, CFC1 distributes its net income of $86.875 to Individual 1. A 10 percent withholding tax is levied on the distribution. The individual elects Section 962 treatment on this income. The results should be as follows:

Therefore, the net proceeds to the US individual when a Section 962 election is made are 66.20 (an effective tax rate of 33.8%. If the election is not made, the amount of the proceeds would be 51.43 (an effective tax rate of 48.57%).

The decrease in corporate rates makes the Section 962 election much more attractive to high net worth individuals and closely held businesses operating overseas than ever before. Companies and their owners should consider reviewing their current structure and calculating the impact a Section 962 election may have for them.

Moore Stephens Doeren Mayhew is familiar with this issue. Contact us. The potential savings are too big to ignore.

[1] For illustration purposes, we have assumed that the CFC has no Qualified Business Asset Investment (“QBAI”)