Common Cash Pooling Arrangements under Attack

Hi There!,

Multinational companies with treasury centers in their structure may need to change the way they do business because of newly proposed debt/equity rules. This can impact not only cash pooling arrangements, but also hedging transactions and intercompany receivables left outstanding too long. There has been pressure put on the Treasury Department to slow the regulation adoption process and make modifications to allow for these type arrangements without running afoul of the regulations. A group of Senate Finance Committee Republicans sent Treasury Secretary Jack Lew a second letter on August 24, 2016 expressing concerns regarding the proposed regulations. This is in addition to various business organizations that have written letters to Congress and the Secretary about their concerns and the speed at which Treasury is trying to finalize the regulations.

Cash Pooling

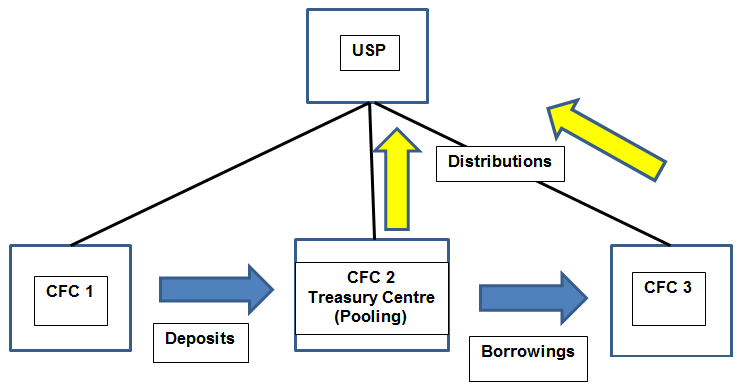

Many multinational companies have set up a subsidiary to pool excess cash in the group and lend to others, often transferring funds on a daily basis. This allows for an efficient use of cash and avoids separate borrowing in each jurisdiction where the company operates. Long-term borrowing would still be made on a separate company basis, but working capital needs would be difficult, expensive and inefficient if required on a separate company basis because of the constant change in funding needs. The documentation requirements that might be needed to avoid falling under these rules would be difficult to comply with because of the constant changes.

A similar issue may result from intercompany sales producing intercompany receivables, especially if these are centralized. Also, in situations where intercompany accounts are not formally offset the company may consider them to be eliminated in consolidation of the financial statements and not clean them up. This is another reason that groups must formally make a payment (even if an offset) on a regular basis and be able to justify the reason the offset or payments are less often than with outside vendors.

Documentation

The extensive documentation requirements of Prop. Reg. Sec. 1.385-3 will apply to cash pooling arrangements. It will also apply to account sweeps, revolving cash advance facilities, overdraft set-off facilities and revolving credit and similar agreements and arrangements. Therefore, each company will have to closely review their operations to determine what types of intercompany funding arrangements might come under these new rules. Failure to properly document an arrangement as debt can result in being automatically classified as equity.

Ramification of Reclassification

The results of having these lending flows reclassified as stock would have ramifications beyond a mere loss of a tax deduction. This would also result in the movement of E&P between entities where (potentially) there had not previously been equity ownership. Also, this would probably be considered non-voting stock, thereby leading to a situation where foreign tax credits (FTC) are moved but cannot be taken as a credit because of lack of 10% direct voting stock ownership (See Reg. Sec. 1.902-1(a)(8)(i) and (a)(3)).

A potential change in ownership (from a reclassification) might also change the results of a reorganization where a certain level of ownership is required for a tax-free transaction. For example, there are certain types of transactions (e.g., Sec. 332) where an 80% direct ownership is required. Before the transaction the test was met, but after a potential audit where the debt was reclassified as stock by a different entity the test would not be met.

The following is a structure where these adverse results might occur:

Contact Moore Stephens Doeren Mayhew to discuss how these proposed debt/equity rules may impact your business.

Sincerely,

Victor (Sandy) Jose, CPA

Director

LinkedIn

Twitter: @MooreStephensDM

For more than 35 years, Victor (Sandy) Jose has assisted clients with their inbound and outbound investments, Foreign Account Tax Compliance Act (FATCA) compliance, Offshore Voluntary Disclosure Program projects, as well as other withholding and reporting projects. Sandy has extensive and broad based global experience in the automotive and manufacturing industries. Contact Sandy at jose@moorestephensdm.com or (248) 244-3082.